CYPRUS TAX OVERVIEW INCOME TAX - COMPANIES

A company is resident in the Republic, tax is imposed on income accruing or arising both from sources in and outside the Republic.

Where a company is not a resident in the Republic, tax is imposed on income accruing or arising only from sources in the Republic.

Resident in the Republic is a company that is managed and controlled in the Republic.

Corporate income tax is 10% flat rate.

Deductible from income are all expenses incurred wholly and exclusively for the production of income.

Such expenses can be Salaries which are subject to social security contributions.

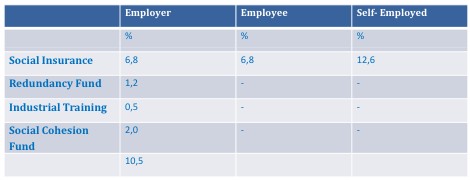

Contributions:

All the above contributions are subject to the upper limit which for 2011 is set at Euro 52.104 note that social cohesion fund has no upper limit.

NON-DEDUCTIBLE FROM INCOME:

- Business entertainment expenses amounts exceeding 1% of the gross income or Euro 17.086 whichever is lower

- Private motor vehicle expenses

- Immovable property tax

- Social Cohesion fund

- Losses

- Losses are carried forward indefinitely

Formation of Cyprus IBC

Cyprus maintains and enhances its competitiveness as a reputable international financial center and distinguishes itself from the infamous tax heavens.

Advantages of Cyprus IBC

Read further advantages for the formation of International Business Companies in the island of Cyprus.